Late last year American Airlines started locking AAdvantage accounts and cancelling pending award travel for people they believe took advantage of a ‘loophole’ to sign up for multiple Citibank credit cards.

Normally there are limits on how often you can get a single card and initial bonus on an AAdvantage Citi card (e.g. not more often than once every 48 months). However new American Airlines frequent flyer accounts were being sent a mailer with a code to apply – and the application process bypassed these restrictions. So people were opening up new accounts, sometimes in the names of their pets, in order to generate mailer codes they could use.

Some people abused this in a scaled-up way, and even sold the miles. Others were caught up in the dragnet who, in my view, didn’t actually do anything wrong.

- they opened an account for their child (real person!)

- they then used the code that came in the mail that specified no restrictions on who could use it

Although everyone that’s contacted me about this, as I’ve asked questions, more of their story comes out than they offered initially and often they stop answering my questions. It seems, anecdotally, that most of the people caught weren’t as innocent as they make themselves appear at first blush – which in no way means there aren’t people who are perfectly innocent.

However if Citi and American Airlines wanted to impose initial bonus restrictions on this application path, they should have done so.

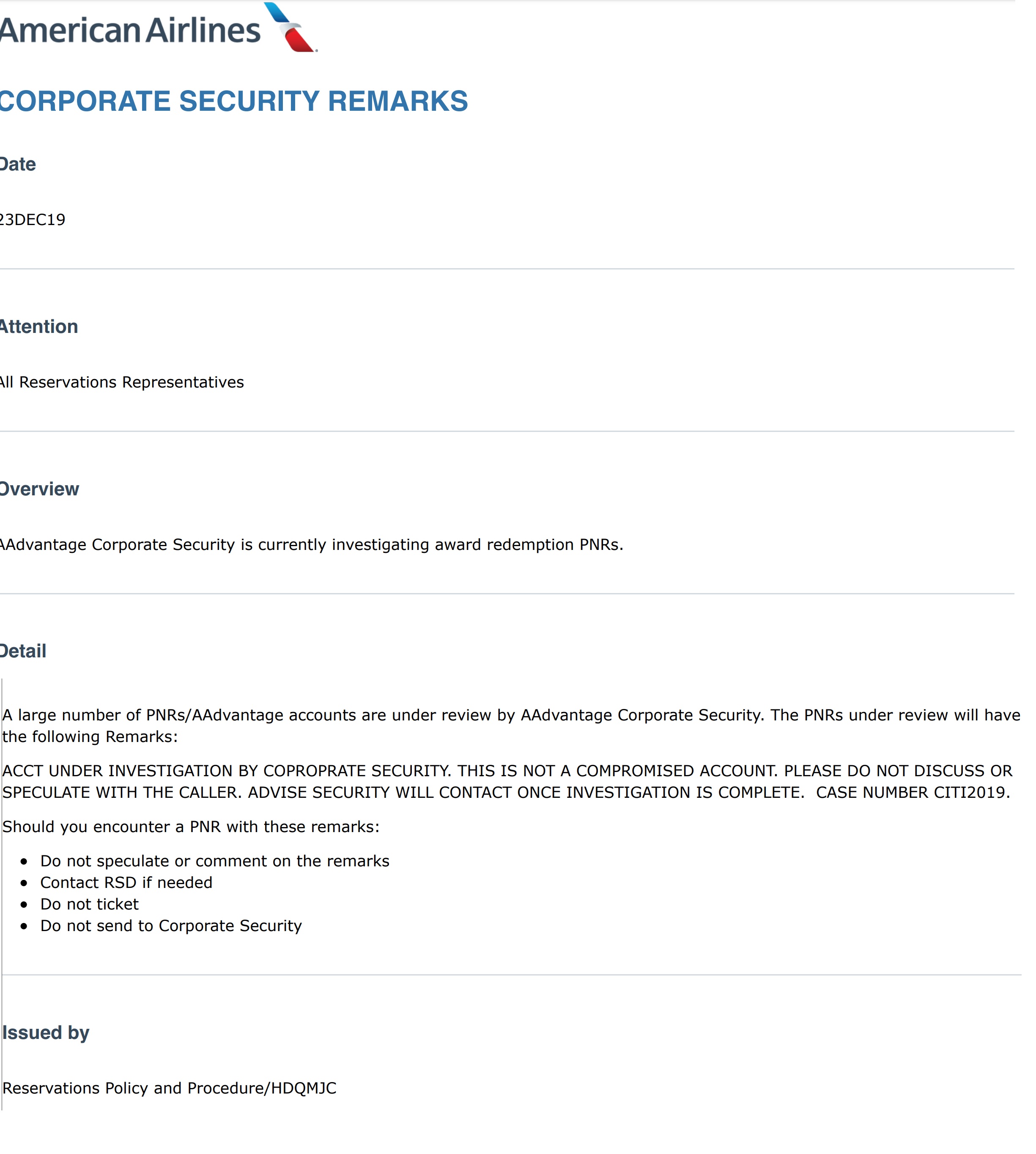

Here’s an internal memo from late last year at American:

Several customers whose accounts were shut down filed complaints with the Department of Transportation. American Airlines has now responded (.pdf download) to a formal complaint that was submitted by Maria Borges. (HT: PaxEx.aero)

American’s response reveals some really detailed sleuthing on their part. But first, the paragraph of American’s regulatory answer that is why they’re going to win: even if there are such people, the complainant isn’t someone innocent getting caught up on a broad sweep.

In fact, between the Complainant, her son-in-law and daughter, 45 Citi Card accounts were opened over a four-year period, entailing more than 1.4 million miles in New Account Mileage Bonuses. The 45 Citi Card accounts do not include an additional nine Citi Card accounts associated with the Complainant’s street address but established under names different than the Complainant, her son-in-law or daughter.

Over a similar timeframe, a further 16 AAdvantage accounts were established by the three of them.10 The 16 AAdvantage accounts do not include five additional AAdvantage accounts associated with the Complainant’s street address but established under names different than the Complainant, her son-in-law or daughter. Of those five additional AAdvantage accounts, two have been terminated due to fraudulent accrual of New Account Mileage Bonuses.

Hoping to avoid detection, the member apparently voluntarily closed their AAdvantage account so that it wouldn’t be audited and award tickets cancelled. When faced with a schedule change they sought to redeposit miles – which they couldn’t do into a closed account, and which they were unable to do into a new account that they opened.

Some interesting things about American’s argument:

- American learned about the tactic by monitoring FlyerTalk and Reddit. Several pages of posts were included in their response as an exhibit.

- They ascribe the lack of a bonus restriction on the application people were using as “due to a technical issue” that “certain unscrupulous individuals” used “to circumvent security protocols.” They say bad facts make bad law, and it’s easy to cast aspersions such as this given the facts of the complaint here.

- American argues that since the standard 48 month language restricting frequency of initial bonuses appears “when accessing the online application via aa.com” that it should be considered to apply to all offers. In fact they argue that someone clicking on an application, and being shown a bonus restriction, is on notice that bonuses are restricted even though future applications contain different restrictions (24 months became 48 months in this case) or no restrictions at all. That’s absurd.

- In another inconsistent claim they argue that “the Citi Card application expressly states that the offers are for first-time account holders” at the same time they acknowledge allowing cardmembers to obtain such offers again after 24 and then 48 months.

- They contend that the restriction on bonuses is part of “Citi’s terms” although of course terms vary by offer and the offers in question contained no such terms which is the point. American’s attorneys seem to be hoping that the DOT will apply a standard seemingly at odds with industry convention and standard understanding of financial regulation.

- American can tell what link someone clicked on to apply for a card. They aren’t fooled by a “.” in a gmail address. They can and will pull call center tapes when it suits their convenience to investigate a DOT complaint (good luck getting them to do it when it supports your position).

- American insinuates that the person filing the complaint isn’t even really the person behind all of this, notes that the complaint was filed without “signature verification” and asks DOT to insist on a re-submission.

To maintain the integrity of the Department’s important procedural requirements, American respectfully requests that the Department promptly direct the Complainant to re-submit a copy of the Complaint dated April 30, 2020, with the signed verification required under § 302.4(b) attached thereto.

Ultimately American argues that the member (1) “engag[ed] in a fraudulent scheme to accrue bonus miles to which the member is not entitled” and (2) “Misrepresent[ed themselves] by opening multiple AAdvantage accounts using false information.”

Their arguments for the first proposition are contradictory and weak. Their arguments for the second proposition are very strong, and all they need to win. Hopefully the DOT won’t be fooled and grant them both sets of arguments.

Great analysis. Well done cutting through the chaff.

Surely American would have been on more solid ground merely asserting that plaintiffs used false information. Even one fraudulent act would surely have given them enough ammo to close all the accounts.

So perhaps their strategy is precisely to use the hard case to make bad law as you suggest.

Most people just used one “identity” to repeatedly apply for cards, so this argument will not protect AA at all. This was a loophole that many people used. Some, like this plaintiff, went beyond and created fake accounts, but most didn’t. It is disingenuous to paint all folks shut downlink el the plaintiff.

The vast majority of those hit are in the healthy middle ground between “created fake AA accounts” and “used their child’s mailer”. They only ever had one AA account, but acquired mailers off Reddit or Flyertalk from complete strangers (perhaps for free, perhaps for anywhere from 5-50$). Sifting through the data, the consensus is that those with 4 or more AA SUBs in two years were eligible to get hit.

It’s hard to see where exactly those in this middle ground broke the T&C — as you point out, nothing says non-transferable in the physically mailed offers (“e-mailers” later had some non-transferable terms) — though it’s hard to say that people doing this were completely oblivious to the risk.

The biggest point of confusion is that even if there was a T&C violation it appears that AA is enforcing what they claim to be Citi’s T&C — and Citi hasn’t provided any support or argument here on behalf of AA in the numerous CFPB complaints filed. I think many assumed if the hammer came down, it would likely be in the form of a ban on applying to Citi cards.

Heck, we got Citi cards for ten years repeatedly without mailers or fake accounts. Many years of AA cards then HH. Now they act like they are really on top of things.It took them two years to figure out what was going on with mailers.

HUCA 19 times to get miles redeposited to a different account than the one booked from sounds like some serious (failed) mileage laundering

Great post!

I used the mailers for my own account. My position is that it was a Citi issue and AA was wrong to cancel my account and repossess the miles I earned previously. Luckily I rarely flew AA so won’t be inconvenienced greatly.

They had to put Clause 1 in there because the overwhelming majority of people didn’t fall under clause 2.

90%+ only had one account. Who knows where they got mailers. Some were bought, some given, some (like in my case) were directly to us, my spouse, or my next door neighbors. And like anyone, there wasn’t any “non transferable” language.

This is a fear tactic and they used one of the most egregious accounts they could find. And they *still* couldn’t prove the miles were earned incorrectly even with thousands of dollars in billable hours writing this response. They could only prove multiple AA accounts were created. They have absolutely no proof (because there is none) towards the other 90%+ and they know it.

You can’t sell miles to Citi, get paid, and then forfeit the miles rendering the cards people paid annual fees on worthless due to Citi knowingly and willingly approving cards. There’s a reason a response from Citi isn’t in this response. One might call AA unscrupulous here, no?

And Gary, what about “Bubbles”? That’s the real question.

Great post Gary!

People that try to scam the system deserve all they get! No sympathy for points whores that take advantage of a legitimate offer to open multiple accounts.

Grow up people and take responsibility! I have 7 cards which I use responsibly but also have gotten the majority of my 8.5 million airline miles from “butt in seat” over 35 years.

No one, IMHO, should be able to game credit cards to get what those that earn the miles the old fashioned way can’t. Glad to see AA, Amex etc clamping down on these clowns

There have been some former and current senior employees of the US Department of Justice — and probably way more mid-level ones — who racked up 1+ Million Mile status on AA from credit card sign-up bonuses alone. I would have to assume there also have been some current or former US DOT employees who had played the credit card sign-up bonus game by applying for a bunch of credit cards to run up the Million Mile counter when those miles all counted toward AA lifetime elite status.

It’s quite interesting that maybe some of the things that were apparently done with aplomb over a decade ago have since become an invitation to be slurred with the label of fraud from some of the very people who racked up hundreds of thousands of miles from credit card sign-up bonuses.

I got my first couple million of AA miles purely from the flights credited to my account and got my status that way. But most of the MM crowd on FT had huge chunks of their lifetime elite status come from credit card sign-up bonuses back when that was still a thing with AA.

You know if you have to parse what you did to the exact nuanced language and all this wiggling, YOU KNOW YOU WERE DOING WRONG!

This claim that AA did not put exactly every little detail in exactly right is ridiculous. This is what creates the “HOT COFFEE” messages on cup, people avoiding COMMON SENSE.

Put this energy into something positive and do something good for the world.

Bottom line, these awards were stolen and taken fraudulently. Stop trying to rationalize it any other way. Adults admit when they did wrong and got caught.

These comments show the lack of ethics, morals, quality, and character of those who did this. They know better, yet chose to STEAL from a company.

AA should look at the total dollars of real damages and file charges for theft against these people.